How I Took Control of My Spending—And Finally Made My Money Matter

Ever feel like your money disappears by the 15th of the month? I’ve been there—paycheck in, bills out, nothing saved. It wasn’t until I hit a breaking point that I realized: budgeting isn’t about restriction, it’s about intention. I started tracking every coffee, subscription, and impulse buy. What I discovered changed everything. This is the real, no-fluff approach I used to gain control, align spending with my goals, and build a financial plan that actually works. It wasn’t fast, and it wasn’t easy, but it was necessary. The truth is, financial peace doesn’t come from earning more—it comes from understanding what you have, where it goes, and why it matters. This is how I transformed my relationship with money, one honest decision at a time.

The Wake-Up Call: When Spending Spiraled Out of Control

For years, I believed I was doing fine. I had a stable job, paid my bills on time, and never missed a credit card payment—at least not more than once or twice. But when an unexpected car repair came up, I froze. I didn’t have the $600 needed, and asking for help wasn’t an option. That moment cracked the illusion I’d been living under: just because I wasn’t in debt didn’t mean I was financially secure. In fact, I was one emergency away from crisis. I sat down and reviewed my bank statements from the past six months, and what I saw shocked me. I earned enough to save, yet my account balance rarely climbed above $200. The truth was, I was living paycheck to paycheck—not because of poverty, but because of poor financial awareness.

It wasn’t one big expense that derailed me; it was the slow drip of small, unnoticed spending. Weekly takeout, online shopping sprees during late-night scrolling, and monthly subscriptions I barely used had quietly eaten up hundreds of dollars. I told myself I deserved it after a long day or that it wasn’t that much. But over time, those small justifications added up to real consequences. I had no emergency fund, no retirement savings, and no clear vision for my financial future. The stress started seeping into other areas of my life—sleepless nights, irritability, and a constant low-level anxiety I couldn’t name. I realized then that money wasn’t just about numbers; it was about peace of mind, freedom, and control over my life.

That moment became my turning point. I stopped blaming my income and started examining my habits. I acknowledged that financial health wasn’t automatic—it required attention, honesty, and effort. I decided to stop pretending I had it under control and began the uncomfortable but necessary work of facing my reality. This wasn’t about shame or guilt; it was about responsibility. And for the first time, I understood that taking control of my spending wasn’t a punishment—it was an act of self-respect. The journey to financial clarity began not with a budget, but with a decision: to stop ignoring the truth and start building a future I could count on.

Mapping the Money: Where Does It Really Go?

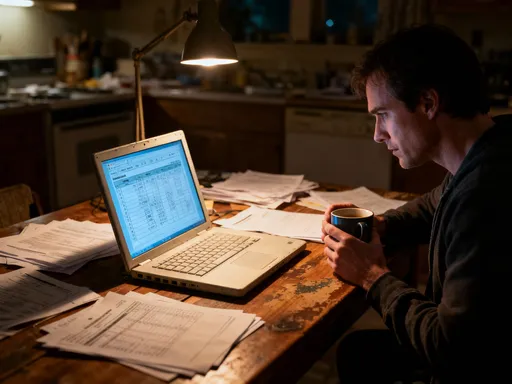

The first real step toward change was gathering the facts. I committed to tracking every single expense for one full month—no exceptions. I didn’t start with a budget or rules; I started with observation. I pulled up my bank and credit card statements and began categorizing every transaction. I used a simple spreadsheet with columns for date, amount, category, and notes. At first, I felt overwhelmed. There were so many transactions I didn’t even remember: $4.50 here for a mobile game, $12.99 there for a digital magazine I’d read once. But as the days passed, patterns began to emerge. I discovered that dining out wasn’t just an occasional treat—it was a near-daily habit, costing me over $300 a month. My streaming subscriptions alone totaled $45, and I was only actively using two of the five services.

One of the most revealing parts of this process was distinguishing between needs and wants. I created categories like housing, utilities, groceries, transportation, insurance, debt payments, savings, personal care, entertainment, dining out, and miscellaneous. As I sorted each expense, I asked myself: Is this essential? Could I get it for less? Do I truly value this? This wasn’t about cutting everything—I wasn’t going to stop buying groceries or paying rent—but about clarity. I began to see that many of my “necessary” expenses were actually choices disguised as obligations. For example, I was paying for premium grocery delivery, but I could save $15 a week by picking up my order instead. Small choices, repeated over time, had a massive impact.

Tracking also exposed my emotional spending. I noticed spikes in online purchases during stressful weeks or after arguments. I’d buy a new sweater or kitchen gadget not because I needed it, but because it gave me a temporary sense of control or comfort. These weren’t large amounts individually, but together they formed a hidden tax on my financial well-being. The data didn’t lie. I was spending over $500 a month on things I didn’t need and barely remembered. That was nearly a third of my take-home pay going toward fleeting satisfaction. Seeing it laid out in black and white was painful, but it was also empowering. Knowledge is the foundation of change. Once I knew where my money was going, I could make informed decisions about where I wanted it to go.

Building a Realistic Budget That Actually Works

With a clear picture of my spending, I was ready to create a budget—but not the kind I’d tried before. My past attempts had failed because they were too rigid, too restrictive. I’d set a $100 grocery limit but ignored the reality of feeding a family of four. I’d ban all dining out, only to break the rule within a week and abandon the plan entirely. This time, I approached budgeting differently. I used my tracking data to build a plan based on my actual life, not an idealized version of it. I followed the principle of assigning every dollar a job—whether it was for rent, groceries, savings, or fun. This method, often called zero-based budgeting, ensures that income minus expenses equals zero, meaning every dollar is accounted for.

I started by calculating my average monthly income after taxes. Then, I listed all fixed expenses—rent, utilities, insurance, loan payments—and subtracted them from my income. Next, I used my tracking data to estimate variable costs like groceries, gas, and household supplies. Instead of guessing, I used the averages from the past month. The key difference this time was including savings as a non-negotiable expense. I treated it like a bill—$200 per month to an emergency fund, $100 to retirement, and $50 to a vacation fund. This shift in mindset was crucial: saving wasn’t something I did if there was money left over; it was a priority built into the plan.

I also included a category for “fun money”—a set amount each month for guilt-free spending on things I enjoyed, like books, coffee out, or small treats. This was essential for sustainability. A budget that doesn’t allow for enjoyment is doomed to fail. By giving myself permission to spend within limits, I reduced the temptation to overspend. I used a digital budgeting tool that synced with my bank account, so I could see my progress in real time. If I went over in one category, I had to adjust in another—no exceptions. This created a sense of ownership and control. The budget wasn’t a prison; it was a roadmap. It didn’t eliminate spending—it redirected it toward what truly mattered to me.

Taming the Triggers: The Psychology Behind Overspending

Even with a solid budget, I knew that behavior change required more than numbers. I had to understand why I spent in the first place. I began to notice that my biggest spending spikes happened during moments of emotional stress. A tough day at work, a disagreement with a family member, or even boredom often led me to open a shopping app or stop by a store on the way home. These weren’t conscious decisions; they were automatic responses to discomfort. I realized I was using spending as a coping mechanism, much like others might turn to food or screen time. The purchase gave me a brief sense of relief or distraction, but it never solved the underlying issue—and it always came with a financial cost.

To break this cycle, I started identifying my personal triggers. I kept a spending journal where I noted not just what I bought, but how I felt before and after. Over time, I saw clear patterns: loneliness led to online shopping, stress led to takeout, and social pressure led to overspending on gifts or outings. Awareness was the first step, but I also needed alternatives. Instead of shopping when stressed, I started going for a walk, calling a friend, or writing in a journal. When I felt the urge to buy something I didn’t need, I implemented the 24-hour rule: I’d wait one full day before making the purchase. In most cases, the urge passed, and I saved the money.

I also redefined my relationship with retail therapy. I asked myself: What am I really trying to feel? If I wanted comfort, could I get it from a warm bath or a favorite movie? If I wanted a sense of accomplishment, could I channel that into a small home project or creative activity? These substitutions didn’t cost money and often provided longer-lasting satisfaction. I learned that emotional spending wasn’t a flaw—it was a signal. It was my mind’s way of asking for care, connection, or rest. By addressing the root need, I reduced the impulse to spend. This wasn’t about willpower; it was about strategy. And over time, I built new habits that supported both my emotional well-being and my financial goals.

Automating Discipline: Systems That Work While You Sleep

One of the most powerful changes I made was removing the need for daily willpower. I set up automatic transfers from my checking account to my savings and investment accounts on the same day I got paid. This ensured that saving happened before I had a chance to spend the money. I also automated my bill payments to avoid late fees and reduce mental clutter. These small systems created consistency without requiring constant effort. I didn’t have to remember to save—I just did, automatically. This approach, often called “paying yourself first,” shifted my mindset from hoping to save to guaranteeing it.

I also adopted a digital envelope system using a budgeting app. I allocated funds to different categories—groceries, dining, entertainment—and once the envelope was empty, I stopped spending in that area for the month. This helped me stay within limits without feeling deprived. For example, if I wanted to go out to dinner, I had to check my dining envelope first. If the money wasn’t there, I chose a home-cooked meal instead. This system gave me freedom within boundaries. I wasn’t banning spending; I was planning it.

Another key tool was setting up sinking funds—small, regular contributions to save for irregular expenses like car maintenance, holiday gifts, or home repairs. Instead of being blindsided by a $300 vet bill, I had been putting aside $25 a month in a pet care fund. This eliminated the stress of surprise costs and prevented me from using credit cards. Automation turned discipline into a habit. I didn’t have to make perfect decisions every day—just set up the right systems once. Over time, these small, consistent actions built a foundation of financial stability. I stopped worrying about money because the systems were already in place to protect me.

Aligning Spending With Long-Term Financial Goals

As my financial habits improved, I began to connect my daily choices to my long-term vision. I asked myself: What kind of future do I want? The answer included financial independence, the ability to travel, and the security of knowing I could handle life’s surprises. I wrote down specific goals: save $10,000 for an emergency fund, pay off my car loan in two years, and contribute consistently to my retirement account. These weren’t abstract dreams—they were measurable targets with timelines.

I started visualizing these goals. I created a vision board with images of a paid-off car, a peaceful retirement cabin, and family vacations. I kept it on my fridge as a daily reminder. Every time I considered an unnecessary purchase, I asked: Does this bring me closer to my goals or further away? This simple question transformed my spending decisions. Saying no to a $50 pair of shoes felt easier when I imagined that money going toward my emergency fund. Small sacrifices became meaningful because they were part of a larger purpose.

I also began measuring my progress monthly. I tracked my savings rate, debt reduction, and net worth. Seeing these numbers improve gave me motivation to keep going. I celebrated milestones—like reaching $5,000 in savings—not with a shopping spree, but with a meaningful experience, like a picnic in the park or a movie night at home. This reinforced the idea that financial success wasn’t about deprivation; it was about alignment. When my spending reflected my values and goals, I felt more in control and more fulfilled. Money became a tool for building the life I wanted, not a source of stress.

Staying on Track: Flexibility, Review, and Growth

No financial plan survives unchanged. Life evolves—paychecks shift, expenses rise, goals change. That’s why I built in monthly check-ins. Every four weeks, I reviewed my budget, compared actual spending to planned amounts, and adjusted as needed. If I overspent in one category, I didn’t panic—I moved money from another or adjusted next month’s plan. This wasn’t failure; it was feedback. I learned to treat my budget as a living document, not a rigid rulebook.

These reviews also helped me catch new spending leaks. For example, I noticed a subscription I’d forgotten to cancel, or a rising utility bill due to seasonal changes. By catching these early, I could make small corrections before they became big problems. I also used this time to celebrate progress. I looked at how far I’d come—how much I’d saved, how much debt I’d paid off, how much more confident I felt. Acknowledging growth kept me motivated.

Setbacks were inevitable. There were months when an unexpected expense derailed my plan, or when I slipped back into old habits. But instead of giving up, I practiced self-compassion. I reminded myself that financial health is a journey, not a destination. One missed goal didn’t erase months of progress. I adjusted, re-committed, and kept going. Over time, my confidence grew. I wasn’t perfect, but I was consistent. And consistency, not perfection, is what builds lasting change.

From Survival to Strategy—Owning Your Financial Future

Looking back, the biggest shift wasn’t in my bank balance—it was in my mindset. I went from feeling powerless to feeling in control. I stopped seeing money as something that happened to me and started seeing it as a tool I could shape. Budgeting became less about restriction and more about intention. Every dollar I spent was a vote for the life I wanted to live. I learned that financial freedom isn’t about having unlimited money; it’s about making your money matter.

This journey wasn’t about extreme frugality or overnight success. It was about small, consistent choices—tracking expenses, building a realistic budget, understanding emotional triggers, automating savings, and aligning spending with goals. It was about creating systems that supported my values and reduced daily stress. Most importantly, it was about reclaiming my time, energy, and peace of mind.

Today, I still enjoy life. I go out to eat, buy things I love, and treat myself. But now, I do it with awareness and purpose. I know where my money goes, and I know why. I have an emergency fund, I’m paying down debt, and I’m saving for the future. I no longer live in fear of the next bill or the next surprise. I’ve turned financial chaos into clarity, and that has changed everything. True financial planning isn’t just about numbers—it’s about designing a life with intention, security, and freedom. And it’s a practice I’ll continue for the rest of my life.