Why I Stopped Chasing Quick Wins and Started Playing the Long Game

I used to think smart investing meant finding loopholes, cutting taxes at all costs, and rushing to maximize returns. But after a costly legal scare with my advisor, I realized my mindset was the real problem. It wasn’t about the strategy—it was about patience, responsibility, and knowing when to slow down. This is what I learned about protecting my money, staying compliant, and building real financial peace—without falling into avoidable traps. What started as a pursuit of efficiency turned into a lesson in humility, one that reshaped not only how I manage money but how I define success. The truth is, many investors like me begin with the same goal: grow wealth quickly and keep as much of it as possible. But in that pursuit, we often overlook the quiet dangers lurking beneath aggressive strategies—the kind that don’t show up on a balance sheet but can unravel everything in an instant.

The Wake-Up Call: When My Investment Mindset Backfired

There was a time when I equated financial intelligence with aggressive tax planning and high-return investments. I believed that the most successful people were the ones who found ways to keep more of their money by minimizing what they paid in taxes. My financial advisor at the time—a confident man with an impressive office and a long list of affluent clients—recommended a series of offshore structures and aggressive deductions that promised significant savings. He spoke in terms of efficiency, optimization, and smart positioning. I listened, eager to believe that I was finally unlocking the secrets of the financially savvy. I signed documents without fully understanding them, reassured by his authority and the promise of lower tax bills. At first, it felt like victory—my returns looked better, my liabilities smaller. I congratulated myself on being proactive, on thinking like someone who truly understood the system.

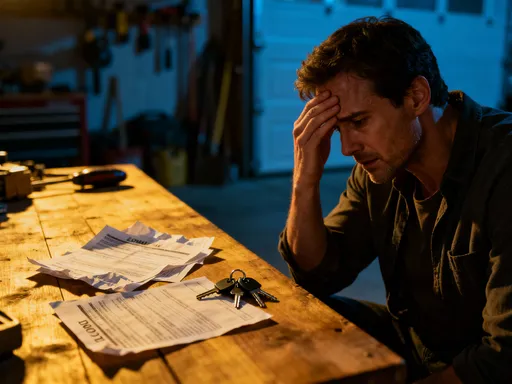

Then came the letter. It was official, typed on government letterhead, and addressed directly to me: I was under audit. The IRS had flagged several of the deductions and structures my advisor had put in place. What followed was a whirlwind of anxiety, confusion, and mounting legal fees. I spent weeks gathering documents, answering questions, and trying to explain decisions I barely remembered making. My advisor, once so confident, became distant, offering vague reassurances but no real defense. I eventually settled the case, paying back taxes, penalties, and interest—far more than I had ever saved. But the financial cost was only part of the damage. The emotional toll was deeper: the loss of confidence, the embarrassment of realizing I had been reckless, and the erosion of trust in my own judgment. That experience was a turning point. I realized that what I had mistaken for boldness was actually naivety. I had confused risk-taking with strategy, and in doing so, I had endangered not just my finances but my peace of mind.

The real lesson wasn’t about tax law—it was about mindset. I had approached investing like a game to be won, not a responsibility to be managed. I wanted quick results and was willing to ignore warning signs to get them. The audit wasn’t just a regulatory event; it was a mirror. It showed me that my definition of financial success was flawed. I had prioritized short-term gains over long-term stability, and in the process, I had compromised the very security I was trying to build. That moment of reckoning forced me to reevaluate everything—from who I trusted with my money to how I measured progress. It wasn’t the end of my financial journey, but it was the beginning of a more thoughtful, deliberate approach.

The Hidden Risk in “Smart” Tax Moves

Many investors fall into the same trap I did: equating tax savings with financial success. There’s a common belief that the smarter you are with your money, the less you pay in taxes. While tax efficiency is a legitimate goal, not all methods of reducing tax liability are created equal. Some strategies fall clearly within the law, while others operate in gray areas that can become dangerous when regulations shift or enforcement intensifies. The line between tax avoidance—which is legal—and tax evasion—which is not—can be thin, and it’s often crossed unintentionally by well-meaning individuals chasing what they believe are clever shortcuts.

Aggressive tax strategies often rely on complex structures, offshore accounts, or interpretations of tax code that push the boundaries of compliance. These may seem appealing, especially when promoted by advisors who emphasize potential savings without discussing risks. But history shows that what appears safe today can be challenged tomorrow. Regulatory agencies like the IRS continually update their scrutiny of tax practices, and courts have overturned strategies that were once widely accepted. For example, certain types of trusts or depreciation methods that were common in the past have since been restricted or disallowed. The danger lies in assuming that because a strategy is popular or recommended by a professional, it is automatically safe.

Another risk is overreliance on a single advisor. Many investors trust their financial planners or accountants completely, assuming that these professionals are monitoring legal developments and acting in their best interest. But advisors have varying levels of expertise, and some may prioritize client retention or commission-based products over compliance. Without independent verification, investors can unknowingly adopt strategies that are outdated, risky, or even illegal. The most dangerous part of aggressive tax planning isn’t the strategy itself—it’s the lack of awareness that accompanies it. When investors don’t understand the mechanisms behind their tax savings, they can’t assess the risks. And when those risks materialize, the consequences extend far beyond financial penalties—they include stress, reputational damage, and a loss of control over one’s financial life.

Legal Advice Is Not Just for the Wealthy—It’s for the Wise

One of the most valuable lessons I’ve learned is that legal consultation is not a luxury reserved for the ultra-wealthy—it’s a necessary safeguard for anyone serious about protecting their financial future. I used to believe that unless I had millions in assets, hiring a tax attorney was unnecessary, even excessive. I thought compliance was something handled by accountants, not lawyers. But I’ve come to understand that tax attorneys bring a different perspective—one focused not just on numbers, but on risk, precedent, and legal interpretation. They are trained to anticipate problems before they happen, to ask the questions that others might avoid.

A qualified tax attorney does more than review forms or represent you in disputes. They help you think critically about your financial decisions. They challenge assumptions and explore edge cases: What if the IRS disagrees with this interpretation? What if a new law invalidates this structure? What if your advisor leaves and no one else understands how this was set up? These are not hypothetical concerns—they are real possibilities that can have serious consequences. By involving legal counsel early, you gain a layer of protection that goes beyond compliance. You gain clarity, confidence, and the ability to make informed choices.

Seeking legal advice is not about fear—it’s about responsibility. It’s about recognizing that financial decisions have legal implications, and that those implications matter. Just as you wouldn’t perform surgery without a doctor, you shouldn’t navigate complex tax strategies without legal guidance. This doesn’t mean every financial move requires a lawyer’s approval, but major decisions—especially those involving trusts, international accounts, or business structures—should be reviewed by someone with legal expertise. The cost of consultation is minimal compared to the potential cost of an audit or legal dispute. More importantly, it reflects a shift in mindset: from chasing gains to prioritizing protection. That shift is what separates speculative behavior from mature, responsible investing.

How Mindset Shapes Your Financial Outcomes

Your beliefs about money are more powerful than any investment strategy. They influence how you interpret risk, how you respond to market changes, and who you choose to trust with your finances. If you view investing as a race to accumulate wealth quickly, you’re more likely to take shortcuts, ignore red flags, and chase high returns without considering the consequences. But if you see it as a long-term journey toward stability and security, you’re more likely to build systems, seek advice, and prioritize sustainability over speed.

My own transformation began when I recognized that my impatience was driving poor decisions. I wanted results fast, so I rushed into strategies without doing proper due diligence. I accepted explanations at face value because they aligned with what I wanted to hear. I dismissed concerns because they threatened the narrative of easy success. That mindset—focused on immediate gains—left me vulnerable to manipulation and error. The truth is, emotional decision-making is one of the greatest risks in investing. It leads to overconfidence, herd behavior, and a willingness to ignore warning signs.

Discipline, on the other hand, means slowing down. It means asking for documentation, getting second opinions, and being willing to walk away from deals that feel too good to be true. It means accepting that some opportunities are not worth the risk, no matter how attractive they seem. The strongest asset you can have in investing isn’t a high-performing stock or a tax loophole—it’s sound judgment. And judgment is built through experience, education, and a commitment to doing things the right way, not the fast way. When you cultivate a mindset of caution, responsibility, and long-term thinking, your financial outcomes improve not because of luck, but because of consistency.

Practical Steps to Avoid Legal Pitfalls in Investing

Avoiding legal trouble in investing doesn’t require extraordinary measures—just consistent, thoughtful habits. The first step is vetting your advisors carefully. Credentials matter, but so does philosophy. Ask your financial planner or tax professional how they approach compliance. Do they emphasize transparency and conservative strategies, or do they promote aggressive tax shelters and complex structures? Pay attention to how they respond to questions about risk. A responsible advisor will acknowledge uncertainty, discuss potential challenges, and encourage independent verification.

Never rely solely on verbal advice. If a strategy involves tax or legal implications, request a written explanation that outlines how it works, what the benefits are, and what the risks might be. This creates a record and forces the advisor to clarify their reasoning. It also gives you something to review with a third party, such as an independent tax attorney. Speaking of which, consider consulting multiple professionals. A financial planner can help with investment strategy, but a tax lawyer can assess legal risk. Having both perspectives increases your chances of making a well-rounded decision.

Keep thorough records of all financial decisions, communications, and documents. Store them securely and update them regularly. If an audit occurs, having organized records can significantly reduce stress and improve outcomes. Most importantly, trust your instincts. If a strategy feels overly complex, too good to be true, or makes you uncomfortable, pause and investigate further. Don’t let fear of missing out override your caution. Prevention is always more effective—and less costly—than correction. By building these habits, you create a framework that protects you not just from legal issues, but from poor decision-making in general.

Building a Sustainable Investment Framework

The most successful investors aren’t the ones who chase every trend or exploit every loophole—they’re the ones who build sustainable, resilient financial lives. This means shifting focus from short-term gains to long-term stability. Instead of asking, “How can I make the most money this year?” ask, “How can I protect and grow my wealth over the next decade?” That small change in perspective leads to very different choices.

A sustainable investment framework prioritizes transparency, simplicity, and compliance. It avoids unnecessary complexity and favors strategies that are easy to understand and maintain. It aligns investments with clear goals—whether that’s funding retirement, supporting family, or leaving a legacy. It accepts that growth may be slower, but it will be steadier and more reliable. Over time, the compounding effect of consistent, legal growth outperforms the fleeting gains of risky maneuvers. A portfolio that grows 6% annually with minimal risk will, over 20 or 30 years, far exceed one that swings wildly between high returns and heavy losses.

This approach also reduces stress. When you know your investments are sound, you don’t lie awake wondering if the IRS will call. You don’t second-guess decisions made in haste. You don’t fear market corrections because your strategy isn’t dependent on perfect timing. Sustainability isn’t about maximizing every opportunity—it’s about minimizing avoidable risks. And in the long run, that’s what allows wealth to endure. True financial strength isn’t measured by the size of your portfolio, but by its resilience and integrity.

The Peace That Comes From Playing It Right

Today, I measure financial success differently. It’s no longer about how high my returns are or how low my tax bill is. It’s about peace of mind. I sleep better knowing that my investments are structured legally, ethically, and with long-term stability in mind. I no longer fear audits or regulatory changes because I’ve built my financial life on a foundation of compliance and transparency. That sense of security is worth more than any quick win I ever chased.

I’ve learned that true financial strength isn’t about how much you keep—it’s about how safely you keep it. The strategies that promise the most often carry the highest risks. The ones that deliver lasting results are usually the ones that seem unexciting: steady contributions, diversified holdings, and conservative tax planning. These don’t make headlines, but they build lives. They allow you to focus on what really matters—family, health, purpose—without the constant background noise of financial anxiety.

By shifting my mindset from aggressive optimization to responsible stewardship, I’ve gained something far more valuable than money: lasting security. I no longer need to prove how clever I am with taxes or investments. I’m content knowing that my decisions are sound, that I’ve done my due diligence, and that I’m building something that can endure. That, more than any return, is the real measure of success. And it’s a lesson I hope others learn before they face the same wake-up call I did.